Financial Planning For Physicians: Your Situation is Unique

What makes your profession unique? You’ve prepared for medical school, had late-night studies, and long shifts, to name a few. Not only does your path stand out, but your financial situation also differs from the general financial planning experience.

A physician can enter the working world right after school and make three figures, while simultaneously holding three figures of education debt. The earning potential of a physician is higher than most other industries, but the financial specifics involve much more than just earnings and debt. Wealth and Financial Planning for physicians require unique considerations and expertise.

When it comes to financial planning – long or short-term – understanding your unique situation will ensure you achieve your financial goals.

The Most Common Financial Planning for Physicians Concerns

Healthcare professionals have an overall higher net worth than most other career paths. Despite physicians’ high net worth and overall earning potential, specific concerns around their wealth often weigh heavier than for other professions. These include:

- Delayed Investment Strategy: Your peers might have chosen different career paths and started investing a few years back.

- Higher Taxes: Higher income can also mean higher tax bracket.

- Litigation Target: Insurance protection needs to go into place regarding malpractice or lawsuits.

- High Education Debt: Build a plan to pay of your debt depending on your specific goals.

- Retirement Planning: A common misconception that you have to clear your debt before you start planning for retirement.

What’s most important to note is that each of these concerns is manageable with proper planning and advice.

How To: Navigate Debt for Physicians

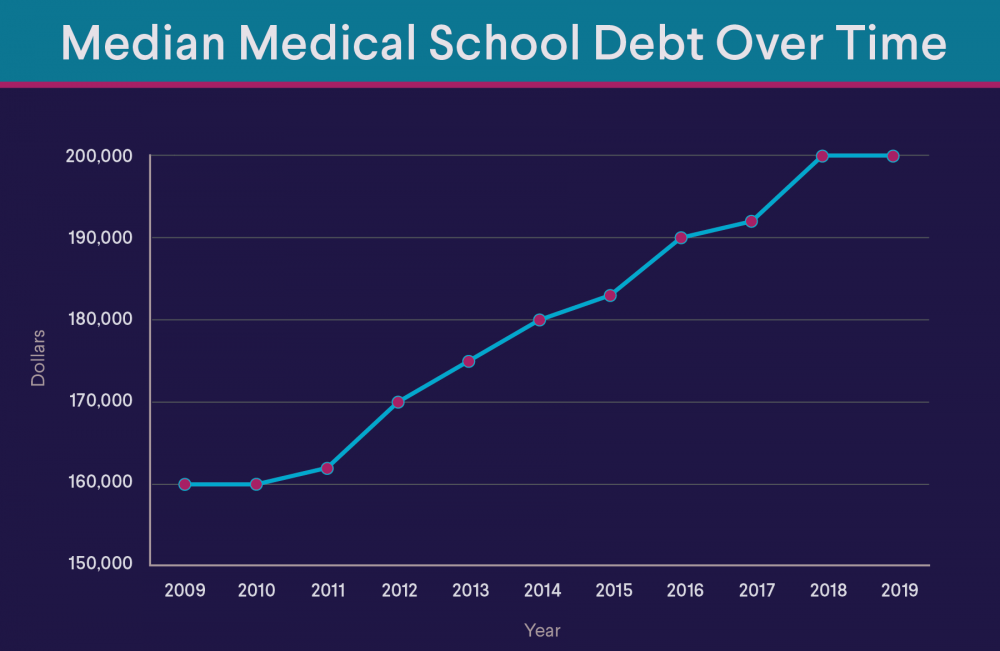

Your net worth is composed of assets and liabilities, and for physicians, there tends to be a big liability when it comes to the cost of education. The graph below shows the average medical school debt over time.

The average medical school graduate owes $250,990 in total student loan debt, 7x as much as the average college graduate.

Depending on your stage in life, there are some strategies you might be eligible for and could explore to make your education debt a little more manageable:

- Deferral Timing

- Loan Forgiveness

- Lower Spending

- Extra Payments

- Income-Driven Repayment

- Refinancing/Consolidation

Regardless of your debt, income, or ultimate financial goals, customized financial planning is the most efficient way to manage your finances and plan for your goals.

Financial Planning for Physicians: The Five Gaps and Five Solutions

Five important pillars of wealth management can impact leaders in higher education (physicians). More specifically, these pillars make you think about the considerations you should have when it comes to your financial wellness.

Asset Location

The right holdings need to be held in the correct place. Depending on your specific financial plan, it’s very likely your Roth IRA should be invested differently than your other qualified accounts (403b, 401a, or 401k). If you have a taxable investment account it should likely be invested differently as well.

Estate Planning

Estate planning, like medicine, is constantly changing. Laws can change on an annual basis when new administrations enter the White House. It’s very common for doctors to shift their careers from state to state over a decade or two. When those changes happen, it’s incredibly easy to put the estate plan updates on the very bottom of the to-do list, which can lead to major concerns.

Long-Term Care Planning

Half of a financial advisor’s clients will tell them they can’t sleep at night knowing they don’t have one, the other half might say they wouldn’t be able to sleep at night knowing they purchased one. No matter what the opinion is, we all deserve financial peace of mind, which is why planning around the concept is so important.

Tax Planning in Retirement

Tax planning is critical in all phases of life, especially when a physician earns the income they’ve worked hard to earn. When you look at where a retired physician earns their living in retirement, we must look at what has been accumulated during all the working years. Commonly you may have amassed a large number of qualified funds and are now looking at very large taxable distributions from those accounts to fund retirement.

The Distribution Phase

The distribution phase is exactly as it sounds, it’s the phase in life after you’ve worked to accumulate your assets and are now distributing those assets to create the life in retirement you have dreamt about. Why is the distribution phase challenging? Simply because picking and choosing where you distribute money throughout your retirement life can be tricky and have adverse consequences if not done correctly.

An Advisor Who Has Your Best Interest

If anyone understands the value of extensive certifications, it’s healthcare professionals. Like medicine itself, financial planning requires a set of very specific expertise and background knowledge. Doctors all over the country have unique circumstances that put each one of them in a different position than their peers.

The fact of the matter is that physicians require a personalized financial plan unique to their situation, in the same manner, their patients require a designed healthcare plan. Working with a Certified Financial Planner (CFP) who can anticipate and understand challenges in financial planning for physicians in order to create a successful outcome, is something that should be considered.

Remember, regardless of your debt, income, or ultimate financial goals, customized financial planning is the most efficient way to manage your finances and plan for your goals.